Markets staged an impressive rebound in the second quarter as a surge in tech-related corporate earnings growth combined with rising hopes for a U.S./Iran ceasefire to push stocks sharply higher, as the major U.S. averages hit new all-time highs.

Markets received positive news almost immediately in the second quarter as, on April 7th, President Trump announced a two-week ceasefire with Iran, ending direct hostilities between the two countries. That news (and the subsequent move lower in oil prices) helped stocks recoup the geopolitically driven March declines, but it was really a stellar first-quarter earnings season that fueled the market rally in April. Annual earnings growth surged to approximately 15% for the S&P 500 following the Q1 results, a number nearly double the long-term average. While AI-linked tech companies posted some of the stronger earnings growth on booming data center demand, a broad swath of companies and sectors posted strong financial results as more than 80% of the companies reporting during the Q1 season beat Wall Street estimates. That AI-led earnings growth, along with the U.S./Iran ceasefire, helped fuel the strong rebound in stocks.

Market gains accelerated in May and were driven by the same factors that drove the April rally: Strong earnings and expectations for a U.S./Iran ceasefire. Earnings in May, while not as plentiful as the April reporting season, were similarly strong with major tech companies such as Nvidia, Intel, Dell, Snowflake and others posting strong results that reinforced the simply massive demand for AI infrastructure. But while the tech sector again posted some of the strongest results, earnings on the whole in May were impressive with Walmart producing solid results and pushing back on fears that higher prices were hurting consumer spending. Meanwhile, surges in demand for data center components such as memory and semiconductors led to massive gains in certain tech stocks through the end of May, as the S&P 500 hit multiple new all-time highs during the month. Geopolitically, while there was no official U.S./Iran ceasefire, markets firmly believed there would be no material escalation either, so the lack of an official agreement didn’t weigh on stocks.

The rally continued in early June thanks initially to reported progress on a U.S./Iran ceasefire agreement, which was signed by President Trump and Iranian leaders in mid-June. Anticipation for the SpaceX IPO (the largest IPO in history) also helped to further support the tech sector and AI-linked investments, as the S&P 500 hit another new all-time high mid-month. However, also in mid-June, investors received a surprise from new Federal Reserve Chairman Kevin Warsh. The Fed made no change to interest rates in June, as expected, but the meeting statement and Warsh press conference were viewed as “hawkish,” and the probabilities for a rate hike later this year rose sharply. That deviation from previous Fed policy expectations caused some market volatility. However, stocks generally proved resilient as falling oil prices (which dropped back to pre-war levels) led investors to believe the current inflation spike will be temporary.

In sum, the stock market completed an impressive rebound from the steep declines of late March, as much-better-than-expected earnings growth (powered primarily by AI-linked tech stocks), continued solid economic activity, and the signing of a U.S./Iran ceasefire helped send the S&P 500 to new all-time highs.

Second Quarter Performance Review

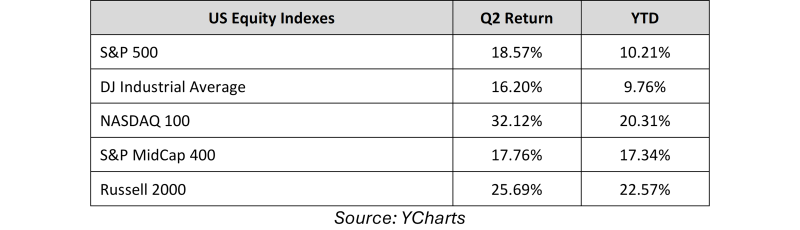

The gains in the S&P 500 in the second quarter were broad, but the impact of the AI boom was evident across and throughout markets.

By market capitalization, small caps outperformed large caps thanks to a combination of strong economic growth (which can disproportionately benefit smaller company earnings), falling oil prices and the “trickle down” of AI optimism towards small-cap tech and AI infrastructure companies.

From an investment style standpoint, growth outperformed value but not as much as one would think given the strength in AI-linked tech stocks in the second quarter. Growth styles benefited from a surge in AI infrastructure stocks such as memory and semiconductor manufacturers while value strategies received a boost from industrials.

On a sector level, 10 of the 11 S&P 500 sectors finished the second quarter with positive returns. The best performing sector in Q2 was, by a very wide margin, the technology sector as it benefited from huge rallies in memory stocks such as Micron and SanDisk as well as continued gains in the semiconductor stocks. Industrials also logged strong gains as companies in that sector were poised to benefit from increased AI data center construction as well as more defense spending. Finally, real estate also posted strong returns on anticipated data center demand, as several tech and AI-linked REITs posted very strong gains in the second quarter.

Turning to the sector laggards, energy was the only sector to post a negative return for the quarter. The energy sector was pressured primarily by falling oil prices as they were sharply higher at the start of April before the U.S./Iran ceasefire process started. The communication services sector was the other clear laggard in the third second quarter (that sector saw only a small gain) as weakness in the legacy internet and mobile providers weighed on the sector (the IPO of SpaceX reminded investors Starlink and other satellite internet providers are legitimate threats to those legacy business models).

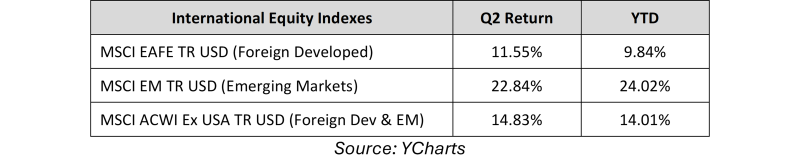

International market performance was also influenced by tech/AI as emerging markets handily outperformed the S&P 500 in the second quarter thanks to an extreme rally in South Korean shares, as they benefited from the boom in memory companies. Foreign developed markets, however, lagged the S&P 500 as they received little AI performance-related boost compared to the S&P 500.

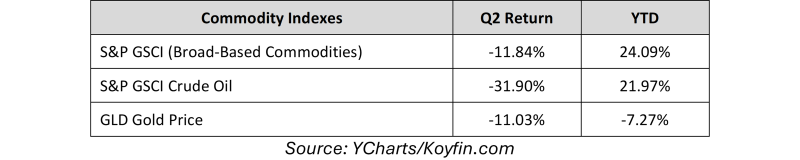

Commodities saw moderate declines in the second quarter, thanks primarily to the drop in oil prices due to reduced geopolitical tensions. Oil prices were volatile but ended the quarter solidly lower on a combination of increased ship transit through the Strait of Hormuz and the U.S./Iran ceasefire agreement. Gold prices also fell during the quarter on the aforementioned decline in geopolitical concerns and a stronger U.S. dollar, which hit a one-year high in June on rising rate hike expectations.

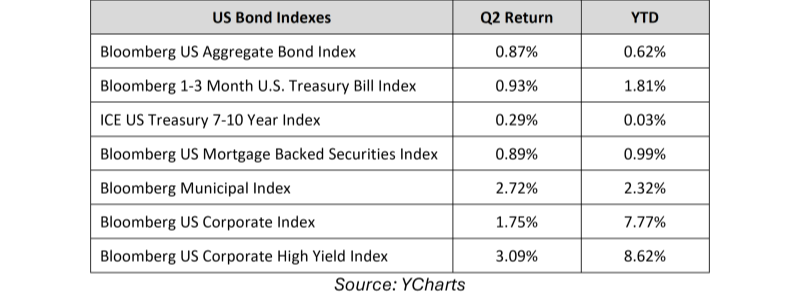

Switching to fixed income markets, the leading benchmark for bonds (Bloomberg U.S. Aggregate Bond Index) realized a modest positive return for the second quarter as falling commodity prices reduced inflation concerns.

Looking deeper into the fixed income markets, shorter-duration bonds again outperformed longer-duration fixed income as some inflation statistics hit multi-year highs and ended Q2 far above the Fed’s 2.0% target.

Turning to the corporate bond market, both investment grade and lower quality but higher-yielding bonds posted solidly positive quarterly returns. High-yield bonds outperformed investment grade debt, as generally resilient economic growth and falling geopolitical risks prompted investors to reach for higher yield despite greater credit risks.

Third Quarter Market Outlook

As they did in 2025, stocks proved resilient in the first half of the year despite several macro-economic surprises, as strong corporate earnings and underlying economic growth overcame doubts about AI profitability, war and higher interest rates.

To that point, investors had to confront numerous market surprises over the first six months of 2026, including a direct war between the U.S. and Iran, a spike in oil prices to multi-year highs, a rebound in inflation (which caused rate hike expectations to replace rate cut hopes) and some doubts about the broad profitability of AI. But while those surprises each caused temporary bouts of market volatility (with the worst coming in March after the U.S./Iran war began), they were largely offset by foundational bull market metrics: Strong earnings and solid economic growth.

The Q1 earnings season was much stronger than expected, and while the earnings gains were led by AI-linked tech stocks such as Nvidia, Micron and others, the reality is the vast majority of companies reported better-than-expected revenue and earnings and that strong corporate performance helped to offset macroeconomic uncertainty.

Economic growth, meanwhile, pushed back consistently on fears of stagflation following the war-driven spike in oil prices. Yes, inflation metrics and prices rose but economic growth never wavered, as virtually all economic indicators from the labor market, manufacturing and service sectors showed solid activity.

Finally, AI enthusiasm remained a key driver of the stock rally, as numerous large tech companies reaffirmed their commitment to spend hundreds of billions of dollars on data center and AI infrastructure buildout, which gave investors continued confidence in the future of AI and provided a broad economic boost, as these massive tech companies spend across the economy to build out data centers and other AI infrastructure.

However, while the market and economy were again impressively resilient in the first half of 2026, we must caution against allowing this resilient market to lull us into a false sense of security as we embark on the second half of the year, because risks to this bull market remain.

First, expectations for Fed rate hikes are rising. At the start of 2026, investors widely expected one or two rate cuts in 2026. Now, because of high inflation, the market is expecting, perhaps, one or two rate hikes. And while that is not automatically negative for markets, the reality is that the last time the Fed embarked on a rate hike campaign (2022) stocks dropped sharply.

Second, the exposure of the entire economy and market to continued AI investment remains a source of concern. Massive AI infrastructure investment is helping to power the economy, but if the companies spending that money begin to doubt the ROI of AI infrastructure investment, they could reduce spending and that would be an economic negative that impacts markets.

Finally, the U.S. economy has proved historically resilient over the past several years, but it is not infallible. The rebound in inflation, if it continues, threatens consumer spending and the housing market and we will be watching the economy closely, because at elevated valuations, the stock market is not at all pricing in a loss of economic momentum.

In sum, we start the second half of 2026 with a strong market: Earnings growth is above historical averages, economic growth is solid and AI enthusiasm remains as boisterous as ever. However, risks remain in the form of high inflation (which could hurt economic growth), potential rate hikes and vulnerability to AI infrastructure spending, and we will monitor these risks closely as we continue to balance risk and reward.

At Fezza Wealth Management LLC, I recognize the risks facing the markets and the economy, and I am dedicated to helping you navigate this investment environment effectively. Successful investing is a marathon, not a sprint, and even bouts of intense volatility are unlikely to alter a diversified approach set up with a goal to meet your long-term investment goals.

Therefore, it’s critical for you to stay invested, remain patient, and stick to the plan, as I've worked with you to establish a unique personal allocation target based on your financial position, risk tolerance, and investment timeline.

I appreciate your ongoing confidence and trust. I will remain dedicated to helping you work toward your financial goals.

Please do not hesitate to contact me with any questions or comments or to schedule a portfolio review.

Sincerely,

Mark Fezza

Securities and advisory services offered through LPL Financial, a Registered Investment Advisor, Member FINRA/SIPC

The Standard & Poor’s 500 Index is a capitalization weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Dow Jones Industrial Average is comprised of 30 stocks that are major factors in their industries and widely held by individuals and institutional investors.

The NASDAQ Composite Index measures all NASDAQ domestic and non-U.S. based common stocks listed on The NASDAQ Stock Market. The market value, the last sale price multiplied by total shares outstanding, is calculated throughout the trading day, and is related to the total value of the Index.

The S&P Midcap 400 Stock Index is an unmanaged index generally representative of the market for the stocks of mid-sized US companies.

The Russell 2000 Index is an unmanaged index generally representative of the 2,000 smallest companies in the Russell 3000 index, which represents approximately 10% of the total market capitalization of the Russell 3000 Index.

The MSCI EAFE Index is a free float-adjusted market capitalization index that is designed to measure the equity market performance of developed markets, excluding the US & Canada. The MSCI EAFE Index consists of the following developed country indices: Australia, Austria, Belgium, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, the Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland and the UK.

The Bloomberg Barclays U.S. Aggregate Bond Index is an index of the U.S. investment-grade fixed-rate bond market, including both government and corporate bonds.

The Bloomberg Barclays U.S. 1-3 Year Government/Credit Index is an unmanaged market value weighted index composed of all bonds of investment grade with a maturity between one and three years.

The Bloomberg Barclays U.S. Mortgage Backed Securities Index is an unmanaged market value weighted performance benchmark that tracks mortgage-backed securities issued by Ginnie Mae, Freddie Mac, and Fannie Mae with 15-year and 30-year maturities. It is a subset of the Barclays Aggregate Bond Index.

The Bloomberg Barclays U.S Corporate High-Yield Bond Index is an unmanaged market value weighted index composed of fixed-rate, publicly issued, non-investment grade debt.

Stock investing includes risks, including fluctuating prices and loss of principal.

The prices of small cap stocks are generally more volatile than large cap stocks.

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly.

The economic forecasts set forth in this material may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification and asset allocation do not protect against market risk.

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise. Bonds are subject to availability, change in price, call features and credit risk.

Bond yields are subject to change. Certain call or special redemption features may exist which could impact yield.

The market value of corporate bonds will fluctuate, and if the bond is sold prior to maturity, the investor’s yield may differ from the advertised yield.

The fast price swings in commodities will result in significant volatility in an investor’s holdings. Commodities include increased risks, such as political, economic, and currency instability, and may not be suitable for all investors.

Government bonds and Treasury bills are guaranteed by the US government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value.